State tax filing obligations are increasingly complex. Businesses can no longer look at payroll and property locations, or other physical presence, as a roadmap to determine their state tax footprints.

States can now easily impose sales, income, and franchise taxes on a business as a result of the 2018 United States Supreme Court decision in South Dakota v. Wayfair, Inc. (Wayfair).

What Is Wayfair?

The Wayfair case involved sales taxes. Following the decision in Wayfair, every state that imposes a sales tax has now enacted economic nexus laws for sales tax. This means a business can be subject to a state’s sales tax even if its only contact with the state is sales to customers.

However, prior to Wayfair, many states enacted economic nexus statutes for income and franchise taxes. As of September 2021, more than 10 states impose income, franchise, and gross receipts taxes on companies solely due to sales that meet a threshold amount.

These include California, Colorado, Massachusetts, Oregon, Pennsylvania, Texas, and Washington. Numerous states also have broad-based economic nexus statutes that impose an income or franchise tax filing obligation if the business derives revenue from sources in the state.

As a result, a business could have income or franchise tax nexus in states based solely on its sales to customers.

What Are the Tax Exposure Risks with Wayfair?

A taxpayer faces heightened risks of exposures from unpaid state taxes, interest, and penalties due because of economic nexus.

The widespread adoption of economic nexus rules by states means that a taxpayer could have unaccrued tax liabilities in states where it conducts business because it’s not filing returns in all states where it has nexus.

A taxpayer could also have risk that a state tax auditor will detect unpaid state taxes in states where it has physical presence nexus because of the increased audit activity by the states due to economic nexus.

These exposures often surface when a taxpayer prepares for an exit event—such as a sale, merger, capital raise, or initial public offering—or receives an inquiry from a state auditor.

If significant, a taxpayer’s state tax liabilities can delay a transaction from closing, add to the advisor fees to resolve or mitigate the issue, and distract its finance and accounting teams from operating the business.

Why Is It Important to Address Historic Tax Liabilities?

Filing a current year return doesn’t cure prior-year tax liabilities. While it’s tempting to simply start filing in a state upon becoming aware of a filing obligation, this approach won’t make the issue disappear because a statute of limitations doesn’t start until you file a return for the tax year. In addition, taxpayers often submit registrations under penalties of perjury, so they must accurately disclose on the registrations when they began doing business.

Therefore, filing a current year return without addressing historic tax liabilities ignores rather than addresses the historic tax exposures.

Instead, a taxpayer should consider the benefits of entering into Voluntary Disclosure Agreements (VDA) with one or more states and localities to address its historic state and local tax liabilities.

What Are the Benefits of Voluntary Disclosure Programs?

Benefits of VDA programs include:

- Limited lookback. Most states limit the number of years that a taxpayer must file to three or four—a significant benefit for a taxpayer operating in a state for many years before becoming aware of a filing requirement.

- Penalty waiver. All states waive penalties for taxpayers that enter a voluntary disclosure program and complete its filing requirements. Penalties often run 10% to 50% of the tax liability and can run up to 100% of the tax liability in certain circumstances.

- Interest waiver. Fewer states waive interest that’s accrued on tax liabilities. For some states, this is an additional offered incentive.

- Financial benefits. State tax reserves reported on financial statements could be released upon resolving liabilities through voluntary disclosure, often resulting in a financial statement benefit because you can eliminate taxes in the years outside of the voluntary disclosure period due to the limited lookback period in addition to abating penalties and in limited instances interest.

- Reduced risk on sale. A taxpayer can show that they identified and addressed prior year exposures, which reduces the time and cost of calculating the liability and negotiating the impact on the purchase price.

How Can VDAs Help E-Commerce Companies?

E-commerce companies may have unknowingly established nexus in multiple states, due to exceeding the sales thresholds established by states. Companies discovering that they have exceeded economic nexus thresholds due to remote sales should carefully consider whether a VDA would benefit them, before initiating filings in a new state. Initiating filings on a prospective basis could result in disqualification from the VDA process. The best approach is for companies to determine their prior years’ exposures first, and then decide which states to approach under the VDA process.

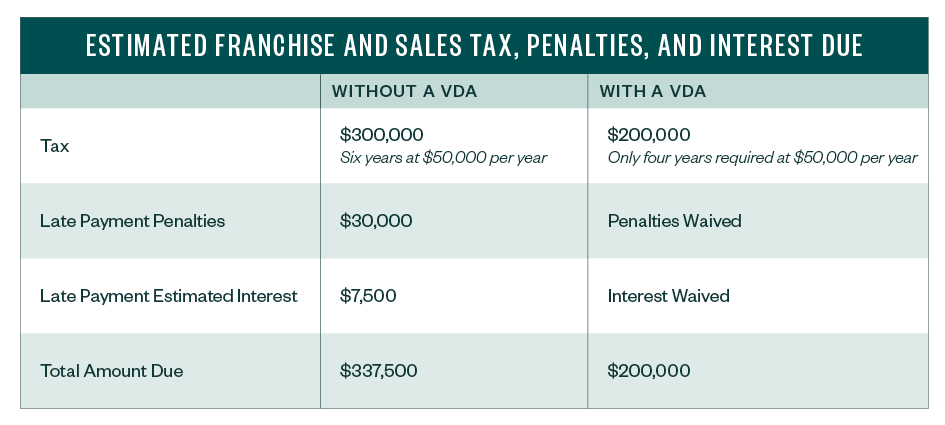

Example

A taxpayer has had a physical presence in Texas for six years. The taxpayer becomes aware that it’s subject to Texas franchise tax and sales tax for all six years. The taxpayer considers applying for a VDA with Texas. For each of the prior six years, the taxpayer’s estimated combined franchise and sales tax liability is $50,000 per year.

Below, the table shows a taxpayer owes Texas approximately 40% less by successfully completing a VDA, as compared to its exposures without a VDA in place.

What Are Next Steps to Pursue a VDA?

It’s important to assess an approach that simultaneously helps mitigate your tax liabilities and fits your business goals.

- Assess state tax footprint. Review your business activities and sales to determine where you have filing obligations.

- Review taxability and sourcing of revenue. An analysis of products or services and determination of each state’s approach to taxing such sales for income, franchise, and sales tax.

- Determine quantification of exposure. Calculate the prior year and prospective tax exposures. Review the state’s tax exemptions and the documentation you need to support a reduction in the taxpayer’s tax.

- Mitigate exposure. Select and prioritize states to approach for VDAs or other steps to mitigate state tax liabilities. At this stage, reduce potential exposures by assessing whether the buyer paid the tax as a result of self-assessment or a tax audit.

- Prepare prospective filings. Develop an approach to meet current and future tax obligations, including registering for tax, software system selection, and implementing compliance procedures.

We’re Here to Help

For questions about how to benefit from or navigate VDAs, please contact your Moss Adams professional.