In May 2014, The Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2014-09, which introduced Accounting Standards Codification® (ASC) Topic 606, Revenue from Contracts with Customers.

The standard, along with subsequent amendments and clarifications issued by the FASB, impacts all professional services companies and will likely have far-reaching effects on their financial reporting and internal control systems.

While the effective date has already passed for public companies, nonpublic entities are required to adopt the standard for annual periods in fiscal years beginning after December 15, 2018, and interim periods within fiscal years beginning after December 15, 2019.

What’s Changing

Under ASC Topic 606, an entity should recognize revenue when it transfers goods or services to a customer in an amount in which it expects to be entitled to receive from the customer.

This new guidance supersedes long-standing, industry-specific guidelines. Much of legacy GAAP is built around a risks-and-rewards notion where revenue is recognized when substantially all the risk of loss from the sale of goods or services has passed to the customer. In contrast, the trigger for revenue recognition under ASC Topic 606 is based on the transfer of control over a good or service to the customer.

As a result, professional services companies will now have to apply significant judgment to determine the timing and amount of revenue recognition involved in their contracts with customers.

How It Works

Using a new five-step accounting process, ASC Topic 606 establishes comparability within financial reporting across industries by applying a uniform framework to revenue recognition. The new guidelines also align GAAP more closely with International Financial Reporting Standards, or IFRS.

The Five-Step Approach

- Identify the contract with a customer

- Identify the performance obligations in the contract

- Determine the transaction price

- Allocate the transaction price to the performance obligations in the contract

- Recognize revenue when or as the entity satisfies a performance obligation

For a detailed overview of the new standard, including best practices for conducting each step in the new five-step approach, read our Revenue Recognition Guide.

Effects

The impact of the new guidance will likely be complex and expansive, involving many different functions within an organization. Here are some of the business areas that may be impacted:

- Financial statements

- Information systems

- Standard contracts and other sales agreements revisions

- Sales incentives and commissions

- Internal control processes

- Executive compensation arrangements

- Debt covenants

- Taxes

Every entity will be effected differently, but in a number of situations, the new standard may result in the following:

- More performance obligations—or separate accounting units—for bundled sales agreements

- Earlier revenue recognition versus legacy GAAP

- Increased deferred and amortized costs in the same periods that revenue is being recognized

- Changes to internal controls, processes, and procedures

- Increased disclosures

- Additional judgement from management

These are generalizations—the exact effects of the new standard may differ for each individual business and should be carefully evaluated.

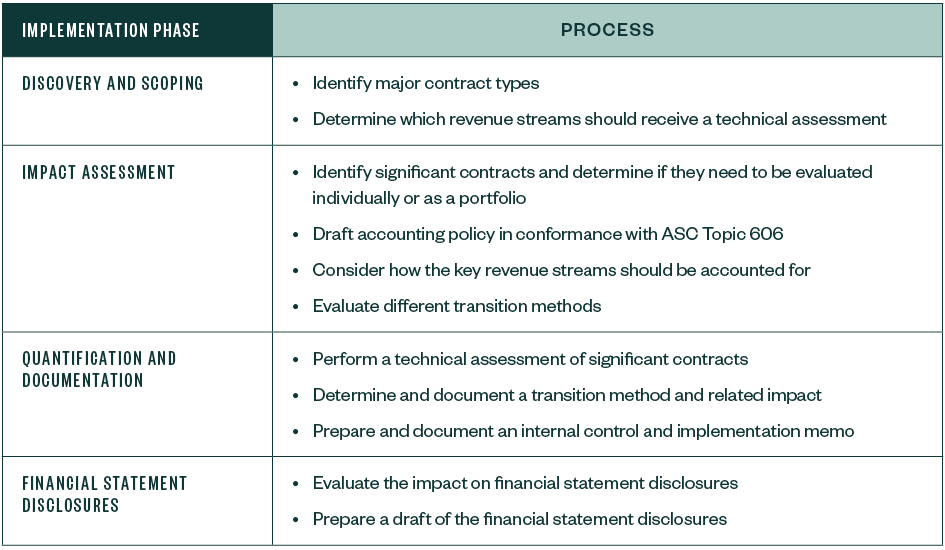

Implementation Timeline

There are four phases of implementation that professional services companies can conduct to help adopt the standard.

Assessing Contract Types

It’s important for professional services companies to begin the implementation process by conducting an inventory of their various contract types and determining which revenue streams require a technical assessment. Completing this step will help define the scope of the project and help management focus on the contracts that will require the most attention.

The following is an overview of the most common contract types professional services companies use and how accounting for the associated revenue may be effected by the new guidance.

Fee-for-Service—Actual Time Incurred

These types of contracts are typically based on the actual time incurred on a project charged at one or more specified hourly rates. They can be short-term contracts, or they can span over multiple reporting periods.

Key Considerations

- Typically, time and materials contracts will follow a similar pattern of recognition as legacy GAAP.

- Revenue will be recognized over time as progress is made towards satisfaction of the performance obligation—or as the services are simultaneous delivered and consumed.

- Management should document considerations as they go through the process because the new guidance relies on judgement.

Approach

- Determine the number of performance obligations. A performance obligation represents a distinct product or service. A promised good or service is capable of being distinct if the customer can benefit from it either on its own or with other readily available resources, and if the promise to transfer a good or service is distinct within the context of the contact.

To determine if a promise is distinct within the context of the contact, it must be determined if the purpose of the promise is to transfer individual goods or services or a combined item for which individual goods or services are inputs. Factors aren’t distinct within the context of the contract if they indicate two or more promises to transfer goods and services. These factors may include:

- Significant integration service is provided that results in a combined output

- One or more of the goods or services significantly modifies or customizes another good or service in the contract

- The goods or services are highly interdependent or highly interrelated

- Allocate the transaction cost. If there’s more than one performance obligation, the transaction price is allocated to each separate performance obligation based on the standalone selling price. This is done on a relative standalone selling price basis at contract inception.

However, if a particular performance obligation isn’t sold on a standalone basis, the standalone selling price will need to be estimated. If pricing for the performance obligation isn’t highly variable or uncertain, the standard states the following two techniques may be used to estimate the standalone selling price:

- The top-down approach—or adjusted market assessment—which considers competitor pricing and market positioning

- The bottom-up approach—or expected cost plus margin—which sets a reasonable margin for production and selling efforts

If pricing for the performance obligation is highly variable or uncertain, the standard allows for the residual approach to be used in select circumstances, where the allocated amount reflects the consideration to which a company expects to be entitled in exchange for a good or service.

Fee for Service—Fixed Fee

A contract that is based on a predetermined, set dollar amount is a fixed-fee agreement.

Key Considerations

- A customer may pay one fee, but there could still be separate performance obligations in the contract.

- Revenue may be recognized over time or at a point in time.

- Management should document considerations as they go through the process because the new guidance relies on judgement.

Approach

- Determine the number of performance obligations. Similar to the actual time incurred contracts discussed above, the number of performance obligations within fixed-fee contracts also needs to be determined. There may be more than one, even if the customer pays a single fee.

- Recognize revenue. Revenue should be recognized when the performance obligation is satisfied and when the customer obtains control over the delivered good or service. For fixed-fee contracts, revenue may be recognized over time or at a point in time, depending on when the customer obtains control of the service or product. Control is generally deemed to be transferred over time when:

- The customer simultaneously receives and consumes the benefits provided by a company as it performs them

- The company’s performance creates or enhances an asset that the customer controls as the asset is created or enhanced

- The company’s performance doesn’t create an asset with an alternative use to the company and the company has an enforceable right to payment for performance completed to date

Companies need to consider all relevant facts and circumstances when determining when control is transferred to the customer, and the pattern of revenue recognition needs to be determined at the beginning of the contract.

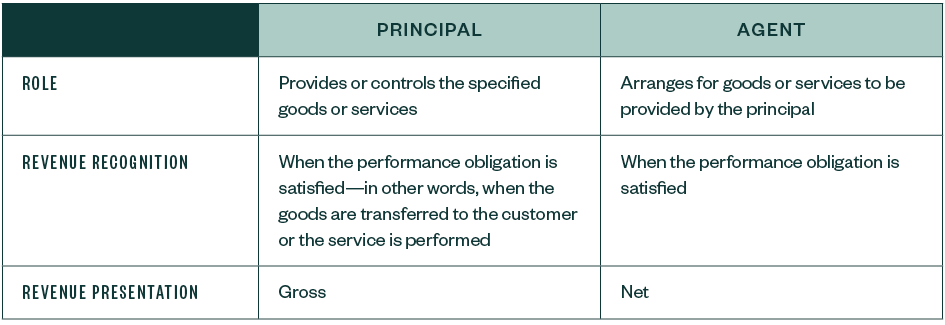

Principal–Agent

If a contract involves a third party providing goods or services to a customer, it’s considered a principal–agent agreement.

Key Considerations

The accounting treatment for principal–agent contracts is mostly consistent with legacy GAAP; however, the new guidance focuses on the concept of control, which is explained in the table below.

Approach

- Establish who controls the good or service. The entity that controls the good or service before that good or service is transferred to a customer is considered the principal and may have the following characteristics: It’s primarily responsible for fulfilling the promise to provide the specified goods or service, has inventory risk before the specified good or service has been transferred to a customer or after transfer of control to the customer, and has the discretion and ability to establish the price for the specified goods or service.

- Identify separate performance obligations. Principal–agent contracts can contain more than one specified good or service, and there can be principal and agent performance obligations within the same contract.

- Recognize revenue when a performance obligation is satisfied. This is true for principal and agent arrangements; however, an entity that is determined to be the principal must recognize revenue in the gross amount of consideration to which it expects to be entitled in exchange for the specified good or service transferred (gross). An entity that is determined to be the agent must recognize revenue in the amount of any fee or commission to which it expected to be entitled in exchange for arranging for the specified goods or services to be provided by the other party (net).

Other Considerations

When determining whether a revenue stream requires a technical assessment, it’s necessary to consider the following.

Variable Consideration

Under the new guidance, variable consideration—such as an incentive, bonus, rebate, or discount—that’s promised within a contract must be considered when calculating the transaction price.

Variable consideration should be calculated using either a best estimate or expected value approach, whichever method is expected to better predict the amount of consideration to which an entity will be entitled. However, variable consideration should only be included in the transaction price if it’s probable a significant revenue reversal won’t occur.

This is a significant change from legacy GAAP and, as a result, some entities may recognize variable consideration sooner under the new standard.

Key Considerations

- An entity should estimate the amount of variable consideration to which the entity will be entitled in exchange for transferring the promised goods or services to a customer. This amount should be reevaluated and updated as necessary during each reporting period over the course of the contact as better estimates become available.

- If it’s probable there will be a significant reversal, variable consideration shouldn’t be included in the transaction price.

- Losses that may result from credit risk shouldn’t be considered when estimating or determining the transaction price.

Approach

- Identify variable consideration—Variable consideration can be explicitly stated in a contract or implied.

- Apply either the expected value method or likely amount method—The expected value is the sum of probability-weighed amounts in a range of possible consideration amounts. An expected value may be an appropriate estimate of the amount of variable consideration if an entity has a large number of contracts with similar characteristics.

The most-likely amount is the single-most likely amount in a range of possible consideration amounts. This means it’s the single most-likely outcome of the contract. The most-likely amount may be an appropriate estimate of the amount of variable consideration if the contract has only two possible outcomes.

Contract Modifications

Management will also need a process to evaluate and document significant contract modifications. A contract modification is an approved change in the scope or price of a contract that creates new enforceable right and obligations or changes the existing enforceable right and obligations.

In some cases, the modification will be treated as a separate contract and won’t affect revenue recognized on the original contract in any way. In other situations, a company will be required to treat a contract modification as a termination of the existing contract and the creation of a new replacement contract. In still other cases, a company will account for a contract modification by recording a catch-up journal entry to adjust the cumulative revenue recognized to date on the contract. The ultimate accounting treatment will depend on the nature of the modification.

Key Considerations

- A contract modification should be accounted for as a separate contract if the scope of the contract increases due to additional distinct good or services and if the price of the contract increases by an amount that reflects the standalone selling prices of the additional promised goods or services.

- If the modification is treated as a separate contract, it won’t impact revenue recognition on the original contract.

- A separate contract will require separate accounting tracking or allocations of costs, billings, and revenue recognition.

- If a contract modification doesn’t meet the criteria to be accounted for as a separate contract, the modification will result in a termination of the original contract. A new contract will be created if the remaining goods or services are distinct from the goods or services transferred on or before the date of the contract modification. If the remaining goods and services aren’t distinct from the goods or services transferred on or before the date of the contract modification, the modification should be accounted for as if it were part of the original contract.

Approach

- Consider whether the contract modification has been approved by all parties

- Determine if the contract modification adds an additional distinct good or service

- Determine accounting treatment based on whether the contract price is derived from stand-alone selling prices for the additional good or service

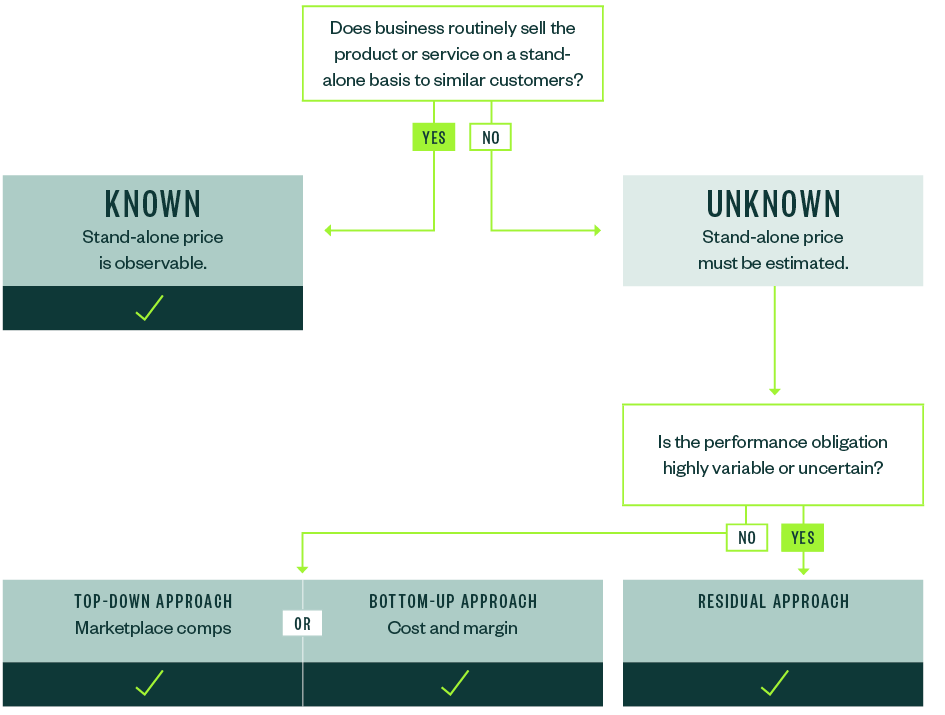

Stand-Alone Selling Price

The process for allocating the transaction price to the distinct performance obligations is similar to what’s done today in many industries and is based on a relative stand-alone selling approach.

Key Considerations

Determining a stand-alone selling price can be straightforward if the business routinely sells the product or service on a stand-alone basis. However, if an entity doesn’t sell a particular performance obligation on its own, it will have to estimate the stand-alone selling price using one of the three methods, as shown in the chart below. These methods are described in detail on page 23 of our Revenue Recognition Guide.

Approach

Capitalization of Costs

Incremental costs of obtaining a contract with a customer within the scope of ASC Topic 606 are deferred and recognized as an asset if the entity expects to recover the costs.

Key Considerations

- Companies can no longer make an accounting election to capitalize or expense costs incurred to obtain a contract; however, a company may elect to immediately expense these costs when the amortization period would have been one year or less.

- Incremental costs of obtaining a contract are those costs an entity incurs to obtain a contract with a customer it wouldn’t have incurred if the contract hadn’t been obtained—such as sales commission.

- Any deferred costs are amortized over the life of the contact—including anticipated renewals as applicable—in the same pattern as revenue is recognized.

- Accounting for liability doesn’t change. Companies will continue to recognize liabilities for incremental costs in accordance with applicable liability guidance.

Approach

- Recognize an impairment loss in earnings if the carrying amount of an asset exceeds its recoverable amount. Under ASC 340-40, the recoverable amount equals the consideration the entity either expects to receive in the future or has received—but hasn’t yet recognized as revenue—minus the costs directly related to providing goods or services that haven’t been expensed.

- Consider the anticipated contract renewal and amendments when determining the amortization period. If there’s ongoing compensation or other expenses based on contract renewals—but not based on the initial contract—it may be necessary to consider if the amortization period should exceed the initial contract period.

Next Steps

No matter where your organization is in the implementation process, it’s helpful to verify the following actions are being taken.

- Assemble a Team

- Understand key differences of the new accounting guidance

- Consider Transition Methods

- Research Disclosure Requirements

ASC Topic 606 contains extensive new disclosures related to a company’s contracts with customers—both quantitative and qualitative.

Revenue is required to be disaggregated into categories that depict the nature, amount, and timing of transfer of goods or services. All entities must also disclose significant judgments made in applying the guidance in ASC Topic 606, including judgments around the timing of satisfying performance obligations, determining the transaction price, and allocating amounts to performance obligations.

This means it’s important to start reviewing the new disclosure requirements now. It may also be helpful to look at public filings for an idea of how companies are implementing the required disclosures.

We’re Here to Help

For more information on how ASC Topic 606 may affect your business, or if you’d like help implementing the new standard, contact your Moss Adams professional.