As the season for year-end tax planning approaches, more of the same means that taxpayers will, at the very least, know what to expect. While there’s been little legislative change this year, recent IRS proposal regulation 2704 could have significant impact for individuals and business owners, if adopted. That said, sound tax planning is essential to effective wealth management, and in today’s tax environment you’ll still want to consider a variety of strategies so you’re well-positioned regardless of tax rule outcomes.

How to Use This Guide

We encourage you to evaluate your options and outline tax planning strategies with your Moss Adams professional sooner rather than later. While it can be tempting to put off thinking about taxes until the last minute, some of the tactics discussed here take time to implement, and your window of opportunity grows smaller as the tax year-end approaches.

In addition to referencing this guide during tax planning season, it can also be a helpful year-round tool. Staying actively involved in these and other underlying areas of tax planning will keep you in a position to preserve and create longer-term wealth for yourself and your family.

Finally, the strategies discussed in this guide are based on current federal tax law. State taxes should also be considered since the tax laws of many states differ from federal tax laws. In light of the evolving tax code, we suggest you visit www.mossadams.com to stay abreast of any changes.

Personal Income Tax

Not much will change in terms of ordinary tax rates in 2016, which will remain about the same as the 2015 rates.

Capital Gains

The maximum 2016 rates for capital gains and qualified dividends remain at 20 percent. If your taxable income falls below the following thresholds, then your maximum capital gains rate will instead be 15 percent:

- For married couples filing jointly, $466,950

- For married couples filing separately, $233,475

- For heads of household, $441,000

- For single filers, $415,051

Regardless of your taxable threshold, the tax rate could potentially rise an extra 3.8 percent if you’re subject to the net investment income tax (NIIT).

With that in mind, here are some planning actions you may want to take:

- Make use of unrealized portfolio losses

- Donate securities with appreciated capital gains

- Time expenditures, such as medical expenses, to shift deductions

- Time year-end property and state income tax payments

Alternative Minimum Tax

The Alternative Minimum Tax (AMT) applies to those who might otherwise pay little or no regular tax because of the use of certain deductions. You’ll need to pay AMT if it results in a higher tax liability than your regular income tax would. When it comes to calculating AMT, many items are not deductible; and in fact they only increase your risk of having to pay AMT instead of regular income tax.

A combination of the following factors—which will vary in effect depending on your individual tax situation—could trigger an AMT liability:

- Large deductions for state and local income or sales tax (particularly in high-tax states such as California and Oregon)

- A large portion of total income from long-term capital gains

- The exercise of incentive stock options (ISOs)

- Personal property or real estate taxes

- Investment advisory fees

- Accelerated depreciation adjustments and related gain or loss differences

- Employee business expenses

- Tax-exempt interest on certain private activity bonds

- Interest on home equity loans not used to build or improve your residence

To reduce your AMT exposure:

- Consider the deferral of payments to the period that provides the greatest tax benefit.

- If you’re planning to exercise ISOs, consult your Moss Adams advisor to avoid unexpected tax consequences, since the exercise might trigger AMT liability and increase your overall tax liability. (See Stock Option Planning below for additional guidance.)

- If you anticipate paying AMT and plan to either purchase a new residence or make improvements to your current residence, consider obtaining the maximum mortgage available if you might otherwise need to borrow the funds later on. Under AMT rules, interest expenses are deductible on only the debts you incur to acquire, construct, or rehabilitate a residence. Additionally, interest expenses on second mortgages are deductible only if they’re used for substantial improvements to an existing residence.

Stock Option Planning

If your compensation package includes stock options, paying close attention to how and when you exercise your options and sell your stock can have a substantial impact on your personal tax liability. Here are a few ways you can control the tax impact:

- Exercise ISOs up to AMT crossover. Assuming you aren’t already in AMT, consider exercising any incentive stock options up to the AMT crossover point, which is the point at which you’ll begin to pay AMT on any additional ISO exercises. By purchasing stock only up to the crossover point, you’re essentially exercising those shares tax-free. Exercise any more, and you’ll end up paying AMT.

- Sell publicly traded shares at a loss. Consider selling the stock if your ISO is for a publicly traded stock, the stock price has gone down, you’ve held it for less than a year, and it doesn’t look like it will recover soon. This will trigger a disqualifying disposition that makes your gains taxable as ordinary income, freeing you from paying AMT on the spread when you exercised. This works best when done within the same tax year (that is, when you exercise early in the year and disqualify by year-end if the stock goes down).

- Exercise nonqualified stock options. If you expect to be subject to AMT for 2016 and don’t expect any AMT credit carryforward, consider exercising nonqualified stock options. In doing so, the accelerated ordinary income may be taxed at 28 percent (the AMT marginal rate) compared to 39.6 percent for taxpayers in the highest marginal federal tax bracket. Plus, all future appreciation will be considered a capital gain. Be sure to weigh your potential tax savings against the opportunity cost of accelerating the income, taking into account the time value of money.

- File an 83(b) election and exercise early. If you’ve received an option grant subject to vesting restrictions and the value of the shares is still equal to the grant price (or strike price), consider exercising your options early, assuming early exercise is available. This will start the capital gains holding clock, getting you to the preferential tax rate on long-term gains sooner. If you do choose early exercise, don’t forget to file an 83(b) election form with the IRS, because there’s a time limit for doing so. Ask your advisor if you have any questions about this.

College Education Planning

Higher education is a significant expense for many families. Taking time to consider how you can use related expenses as a tax advantage is well worth the effort.

- Claim the American Opportunity Tax Credit. This credit is available for the first four years of qualified expenses paid for undergraduate education. For tax year 2016, you may be able to claim up to $2,500 per student. Of the credit amount you receive, 40 percent is refundable.

- Explore other credits and deductions. If you’re paying for postsecondary education and aren’t eligible for the American Opportunity Tax Credit, you may still be eligible for the lifetime learning credit or the tuition and fees deduction. Consult your Moss Adams professional to determine your eligibility.

- Create a Section 529 account. These investment accounts can be used to accumulate funds for college-related expenses. The appreciation on the investments within the account is tax-free for qualified distributions. Under certain elections, taxpayers may contribute up to $70,000 (for single filers) or $140,000 (for married couples) to a Section 529 account in one year without reducing their lifetime gift and estate tax exemption, although you should contact your tax professional regarding gift tax filing requirements. If you currently maintain college funds in taxable accounts, it may make sense to shift these funds to a Section 529 account, where they won’t generate future taxable income.

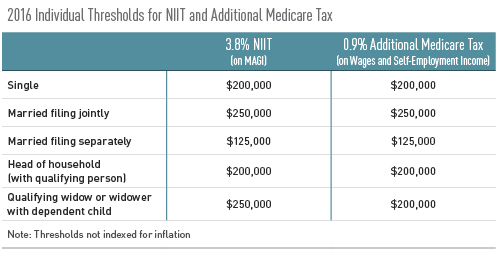

Net Investment Income Tax and Additional Medicare Tax

Now in their third year, the 3.8 percent NIIT and additional 0.9 percent Medicare surtax apply to taxpayers with income above certain thresholds. The thresholds for the two taxes are nearly the same, but they apply to different types of income.

The 0.9 percent additional Medicare tax applies to Federal Insurance Contributions Act wages and self-employment income. The NIIT equals 3.8 percent of the lesser of the taxpayer’s net investment income or the amount by which the taxpayer’s modified adjusted gross income (MAGI) exceeds the thresholds.

Net investment income includes interest, dividends, capital gains, rents and royalty income, income that isn’t from a trade or business, and any other passive business income (meaning the taxpayer doesn’t materially participate in the business).

Certain types of income are excluded from net investment income, including wages, self-employment income, active trade or business income, retirement plan distributions, unemployment compensation, Social Security benefits, alimony, interest from tax-free bonds (such as municipal bonds), and Alaska Permanent Fund Dividends.

Note that the thresholds aren’t indexed for inflation, which means they haven’t changed from last year or the year before. It also means that inflation alone will cause these taxes to reach increasing numbers of taxpayers over time.

Limiting Your Tax Exposure to the NIIT

Higher-income taxpayers should evaluate their liability for both the NIIT and the additional Medicare tax. If one or both taxes may apply, consider adjusting your withholding amount or estimated tax payments to account for the increase. Here are some other ways to limit your tax exposure to the NIIT:

- Time deductions and losses

- Prepay state income tax

- Reconsider investments that generate passive income

- Maximize your retirement contributions

- Use like-kind exchanges—these kinds of transactions in place of cash can defer triggering taxable gains in rental or business real estate

- Use the installment method

- Revisit activity participation levels

- Gift income-producing assets to children

- Distribute trust income

- Incorporate as an S corporation

Real Estate Holdings

With real estate markets recovering across the country and prices on the rise, opportunities to save related tax dollars are critical. Work with your tax professional to utilize energy incentives or make a Section 1031 exchange.

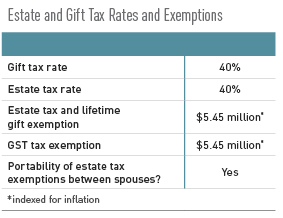

Estate and Gift Planning

With permanent rates now in effect for estate, gift, and generation-skipping transfer (GST) taxes, estate planning may seem less challenging; however, remember that this permanence is relative—in the tax world, it means only that there are no expiration dates. Congress could still pass legislation to alter today’s rates and rules.

The Highway Act

The 2015 Highway Act (see below) included a few key changes for individuals with regard to gift and estate taxes. Notably, it implemented a new basis consistency standard. Generally, the tax basis of property received by a person upon another’s death can’t exceed the value of that property as reported for estate tax purposes. The change requires that an executor provide values used in the estate to the person receiving the property. This revision is effective for property reflected on estate tax returns filed after July 31, 2015.

IRS Proposal 2704

On August 2, 2016, the IRS released proposed regulations that would strengthen its goal of significantly reducing valuation discounts for transfers of minority interests among family members in closely held businesses and investment entities—such as family limited partnerships. A public hearing is scheduled for December 1, 2016.

If adopted, the new regulations won’t be effective until the publication of a Treasury Decision formally adopting the final regulations, but the regulations could be adopted as early as December 31, 2016. Now is the time to evaluate your estate and gift strategy for transferring your closely held business under current rules rather than being negatively impacted by any future final regulations.

For more information, see our recent alert and discuss with your tax advisor.

Lifetime Gifts

In 2016, the amount you can give during your lifetime without incurring any gift tax has increased slightly and is currently set at $5.45 million (with an annual exclusion of $14,000 per recipient). This amount will be indexed for inflation annually. The gift tax rate on gifts greater than $5.45 million is 40 percent. If you plan to give, consider the following methods for reducing your tax exposure:

- Take full advantage of the $14,000-per-recipient annual exclusion. Remember that your spouse can also gift $14,000 per recipient.

- Plan the timing and type of gifts. When considering lifetime gifts above the annual exclusion, plan carefully to chart a tax-efficient course of action while considering your personal cash flow needs and long-term estate planning goals.

- Mind state inheritance tax issues. Some states have an inheritance tax of their own, and the exemption amount can be much less than the federal amount ($5.45 million).

Low Interest Rate and Valuation Opportunities

- Refinance family loans. Applicable federal rates (AFRs)—which are the minimum interest rates that must be charged for bona fide loans between related parties—remain at generally historic lows. As such, it may be possible to refinance loans between family members or with a closely held business, significantly reducing interest payments.

- Transfer wealth through trusts and leverage. The $5.45 million gift tax exemption, combined with historically low AFRs, creates an opportunity to transfer large amounts of wealth to your heirs through the use of leverage and certain types of trusts.

- Transfer assets before they rise in value. If you’re holding any assets you believe will increase in value quickly, consider making a lifetime gift to (or a lifetime sale for) your beneficiaries now, before the values jump up significantly.

Gifting and Trust Entity Structures

- Contribute property to a family-controlled entity. A family limited partnership (FLP) is the preferred vehicle for this tax-saving technique. It provides the senior member continued control of the assets held in the FLP while gifting a portion to the next generation.

- Form a grantor-retained annuity trust (GRAT). In this technique, a grantor gives an asset to a GRAT. In turn, the GRAT pays the grantor an annuity stream based on the current value of the asset. The annuity is a fixed amount determined after the value of the assets is set.

Developing or Updating Your Estate Plan

In addition to the specific estate and gift planning opportunities previously covered in this section, remember that the end of the year is an ideal time to revisit your plan as a whole (or create one, if you don’t already have one). Here are a few of the items to cover:

- Understand and revisit your goals

- Confirm powers of attorney are in place and wills are up to date

- Plan for transition

- Understand how federal and state estate tax laws will affect you

Charitable Giving

Making a charitable contribution may entitle you to an income tax deduction in the year you make the gift. Most deductible contributions are those made to US organizations described in Section 501(c)(3) of the Internal Revenue Code. This includes not-for-profit entities organized and operated for charitable, scientific, educational, religious, and other purposes. Contributions to nonqualifying charitable organizations aren’t deductible. A few tax-saving opportunities to consider when engaging in charitable activities:

- Examine any volunteering activities and expenses

- Gift appreciated or depreciated property

- Plan the timing of larger charitable gifts

- Account for charitable deductions in AMT calculations

- Use credit cards and checks to squeeze in final 2016 deductions

- Choose a recipient later using donor-advised funds

Charitable Giving as Part of Your Overall Estate Plan

By incorporating your charitable contribution planning into your long-term estate plan strategy, you can help increase cash flow for yourself and your heirs while achieving your charitable goals.

- Consider setting up a charitable remainder trust. If you plan to make sizable donations, this will allow you to take the deduction when you fund the trust; the remaining assets will be passed to charitable organizations at the end of the trust term. Properly structured and administered, the trust can also accumulate greater assets without incurring a tax burden, since the trust is tax exempt.

- Designate charitable organizations as retirement account beneficiaries. In doing so, assets held in accounts such as 401(k)s and IRAs fund your charitable bequests while reducing income and transfer tax consequences.

- Keeps tabs on complexity. Direct contributions to qualified organizations, donor-advised funds, and charitable trusts each come with their own complexities and costs. As a donor, balance the size of the charitable contribution with the complexity of the gifting vehicle.

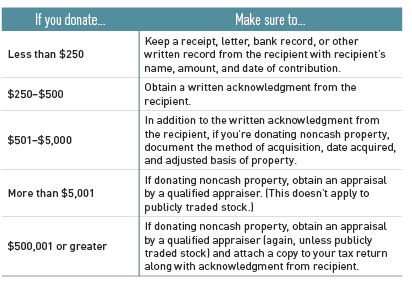

Document Your Charitable Contributions

As you execute your charitable gifting plan—even if you haven’t formally created one— remember that you’re only able to take advantage of potential tax deductions to the extent that you document them effectively. To that end, adhere to the following guidelines:

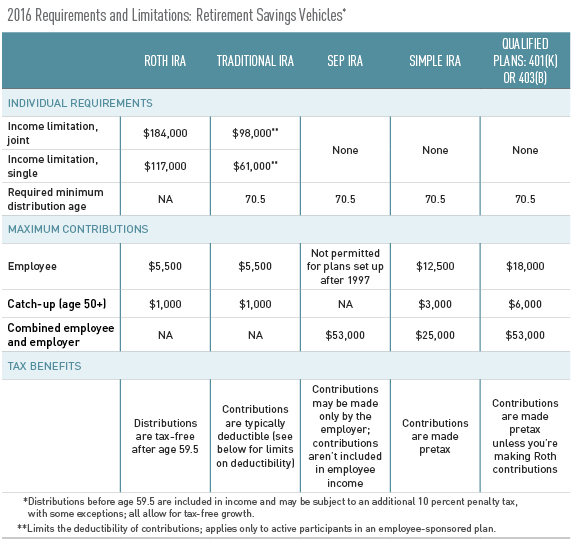

Retirement Planning

Taxes can be a key factor in retirement planning. The tax-related decisions you make now and throughout the course of your career will affect how much you’re able to save for your retirement and through what means.

Things to consider:

- Establish certain plans before year-end. Keogh plans, 401(k) plans, and certain others allow larger tax deductions, but they must be established by year-end—even though contributions don’t need to be made by that time. If you’re considering options for a company sponsored retirement plan, be sure to have it in place before December 31.

- Weigh the benefits of a Roth IRA. Any taxpayer can now convert a traditional IRA to a Roth IRA, regardless of income (AGI). Certain qualified plans may allow for an “inside the plan” conversion, which should also be considered where appropriate.

- Watch for penalties with multiple IRA rollovers. Established January 1, 2015, the once-a-year limit on IRA rollovers that aren’t direct custodian-to custodian transfers will apply to all your IRAs in aggregate rather than to each one separately.

- Employ children to jump-start retirement savings. If a child has earned income, there are strategies he or she can use to contribute to a traditional or Roth IRA. Where practical, consider employing children in the family business to generate earned income. Those earnings can be contributed or funds could be gifted into the IRA accounts.

- Contribute to a myRA account. Finalized in December 2014, this is a low-risk, Treasury-backed Roth IRA investment account intended for beginner retirement savers who don’t otherwise have access to an employer-sponsored plan.

- Check your employer plan. Be sure you’re maximizing your contribution to any retirement plan programs your employer may sponsor and receiving the full employer matching contribution if there is one.

Wealth Management

While tax planning shouldn’t be the sole driver of investment decisions, it can play an important role in preserving and generating investment returns, growing your assets, creating sustainable income, and achieving financial security. The decisions you make today and throughout the course of your career can affect your short-and long-term investments as well as your taxes. Seek advice from both a tax and investment perspective so you can rest assured, knowing the two are aligned with your wealth management goals.

Investment Management and Strategy

- Account for the impact of state taxes. When selecting municipal bonds for the federal tax- free interest income, consider the impact of state income taxes as well.

- Stay disciplined. With interest rates stuck at historically low levels, avoid the temptation to change your investment risk profile solely to search for potential increased yield.

- Consider realizing losses. Work with your investment advisor to manage net capital gains and utilize any unrealized capital losses that may be in your account (tax-loss harvesting).

- Reduce capital gains. Consider making your charitable donations using appreciated investments to avoid paying capital gains taxes on those holdings.

- Reevaluate and rebalance portfolio. Given recent equity market performance, review your investment strategy to determine whether your asset allocations remain consistent with your personal goals and if it’s time to rebalance your portfolio.

- Evaluate the impact of the NIIT. Reevaluate tax-exempt yields versus taxable yields in light of current market conditions and the 3.8 percent tax.

Personal Financial Planning

- Create or update your personal financial plan. For those without a plan, take the time to set clear short- and long-term goals, and begin to monitor your progress toward those goals.

Insurance

- Reevaluate your needs. Update your policies to ensure they’re still in accordance with your current needs, transfer goals, and liquidity concerns. Pay particular attention to policy type, coverage amounts, ownership, and beneficiary designations.

- Check in on policy performance. Review your existing insurance policies, including annuities, to confirm they’re performing as expected and operating efficiently.

- Review employer-owned policies. If you purchased a new employer-owned life insurance policy, confirm that the required formalities are being followed. If not, the proceeds could become taxable income when received, increasing the corresponding tax liability.

International Considerations

Understanding the tax implications of cross-border transactions and investments is even more critical today than ever before. For example, US taxpayers living outside the United States need to be alert to special issues in estate planning, and US citizens with noncitizen spouses have issues of their own to address. Increasing numbers of Americans live, work, and—especially—invest abroad, activities that may create a host of filing requirements and potential traps for the unwary. Significant and frequently negative tax issues may also be created when individuals immigrate to or expatriate from the United States.

The following considerations may help you reduce your tax burden and risk:

- Consult with your advisor regarding any foreign mutual fund investments. Investing in a foreign mutual fund or passive foreign investment company (PFIC) may essentially double your tax burden related to gains or income from the investment compared to a non-PFIC investment unless you make certain elections; in fact, in some situations it creates significant tax liabilities when no economic gain has actually been realized.

- Review tax amnesty program options. The IRS recently made several changes to the Offshore Voluntary Disclosure Program, the Streamlined Foreign Offshore Procedures, and the Streamlined Domestic Offshore Procedures. These programs are designed for US taxpayers who have unreported foreign income for prior years or who haven’t submitted all the required disclosure forms to the IRS.

- File a US tax return, even if you’re overseas. Unlike most nations, the US requires citizens residing outside the United States to file annual US income tax returns and to pay tax on their worldwide income.

- Understand the US foreign disclosures requirements. US citizens, green card holders, and US tax residents who make or hold foreign investments may have a number of disclosure requirements even if there aren’t any current tax consequences. Some of the most common foreign disclosures forms are:

- Foreign Bank Account Report—FinCen 114

- Statement of Specified Foreign Financial Assets—Form 8938

- Transfer of property to a Foreign Corporation—Form 926

- Controlled Foreign Corporation—Form 5471

- Controlled Foreign Partnerships—Form 8865

It’s important to understand and comply with the foreign disclosure requirements as many of these carry a minimum $10,000 penalty for failure to file.

Additional Considerations

Self-Rental Planning and Pitfalls

Business owners commonly acquire real estate that they then lease to their businesses. These function as investment assets, and they’re often owned by a legal entity, such as a limited liability company (LLC), separate from the business for a variety of legal, financial, tax, and personal reasons. One common benefit of rental real estate ownership is the tax losses it generates as a result of depreciation, mortgage interest expense, real estate taxes, and other property maintenance expenses—particularly in the early years of ownership.

Despite the routine nature of these arrangements, it comes as a surprise to many that these tax losses may not be immediately deductible against other sources of income, such as wages, capital gains, or business income.

The Highway Act

On July 31, 2015, President Obama signed a new law called the Surface Transportation and Veterans Health Care Choice Improvement Act of 2015, also known as the 2015 Highway Act. This new law revises due dates for partnership and corporate tax returns, revises the extension rules for certain types of entities, allows extensions for foreign bank account reports, sets a new basis consistency standard, and makes changes to mortgage information returns.

The largest change is a restructuring of business entity tax return due dates, generally effective for business tax returns for tax years after December 31, 2015, which means the following due dates will impact your 2016 tax returns (that is, the 2017 filing season):

- Partnership tax returns will now be due the 15th day of the third month after the end of the tax year. (Under preexisting tax law, returns were due the 15th day of the fourth month.)

- C corporation tax returns will be due by the 15th day of the fourth month after the end of the tax year. (Under preexisting tax law, these were due on the 15th day of the third month).

- For C corporations with fiscal years ending June 30, the change won’t go in effect until after December 31, 2025.

Tangible Property Regulations

The final tangible property regulations— issued by the IRS in two installments in September 2013 and September 2014—are effective for tax years beginning on or after January 1, 2014. They apply to all taxpayers that acquire, produce, or improve tangible property.

- Review your compliance with the new regulations. With the mandatory effective date already behind us, it’s imperative that business owners understand the impact of the regulations on their company. Create an implementation and ongoing compliance plan as soon as possible to avoid filing-season surprises or to potentially identify tax-planning opportunities related to the new regulations. Review your asset capitalization policies to see that they’re in compliance with the new regulations and consult with your Moss Adams professional for help identifying opportunities and implementing necessary changes.

Business Credits

A number of business tax credits and incentives are available in 2016 to help you reduce what you owe. In addition to those listed here, be sure to consider hiring and zone-based credits as well as those available at the state and local level.

- Claim small-employer health insurance credits. Eligible small employers are allowed a credit for 50 percent of certain contributions made to purchase health insurance for their employees. Eligible employers are generally those with 10 or fewer full-time equivalent employees with wages of $25,000 or less that offer a qualified health plan through a Small Business Health Options Program exchange.

- Take advantage of the employer-provided child care credit. Employers can claim a credit of up to $150,000 for supporting employee child care or child care resource and referral services. This provision has been extended permanently.

- Explore R&D tax credits. If your organization develops new or improved products or processes, it may be able to benefit from federal and state (where applicable) R&D tax credits. The R&D tax credit is a dollar-for-dollar credit against taxes owed or paid.

Employee Benefits

Offering a variety of benefits can help you attract and retain the best employees— and it could help you save tax dollars.

- Amend documents to allow in-plan Roth rollovers. If your company offers a 401(k) or 403(b) plan, you can now amend them so that participants can convert them to Roth plans, which may be more tax-efficient for some. Some governmental 457(b) plans also allow in-plan Roth rollovers.

- Extend cost-free retirement savings options through myRA. Finalized by the Treasury Department in December 2014, the myRA program is a no risk, Treasury-backed Roth IRA intended for beginner retirement savers who don’t otherwise have access to an employer-sponsored plan.

- Consider verifying the marital status of employees. For employees who don’t notify you of a marital status change following Obergefell v. Hodges, you may want to consider checking into whether they’re engaged in legal marriages or domestic partnerships. Obergefell was a Supreme Court case that decided in 2015 that same-sex couples had the fundamental right to marry.

Health Care Reform

A number of Affordable Care Act provisions in addition to the Net Investment Income Tax, or NIIT, and Medicare surtax will impact individuals and families that don’t receive health insurance under an employer’s plan.

- Gather documentation to substantiate your 2016 coverage. Starting last year, insurance companies are required to report the coverage provided to health insurance policyholders on the new Form 1095-B. Employers will report whether they offered minimum essential coverage to their employees on Form 1095-C. Employers with self-insured health plans may choose to report both insurance offered and the coverage actually provided on a single Form 1095-C by filling out Part III of that form.

- Renew or purchase your 2017 coverage. Marketplace coverage for 2016 ends December 31, 2016. You can either renew your existing health plan or choose a new plan via the marketplace during the 2016 open enrollment period, which opened November 1, 2016, and ends January 31, 2017.

- Be aware of penalties. The health care mandate penalty for not having health insurance in 2016 went up 2.5 percent of household income (capped at the annual premium for the national average Bronze plan sold through the marketplace) or $695 per adult plus $347.50 per child under 18 years old (capped at $2,085). Starting in 2017, the penalties will increase each year by a cost-of-living adjustment. If an individual wasn’t covered for every month of 2016, they may still be able to avoid paying penalties if they qualify under one of the available exemptions including short-term gaps in coverage when switching jobs or for certain financial hardships. Please contact your Moss Adams professional to discuss this further.

Exit Planning

As a business owner, exit planning is a major, one-time opportunity that warrants your long-term attention. It also requires a long-range planning horizon. Understanding your strategic options for exiting your business will keep you in a position to extend your business’s value and legacy while preserving the wealth you’ve generated for your future. Consider your exit in terms of the following basic strategies:

- Keep your business in the family. You can transfer ownership of your business by gifting or selling your ownership interests to other family members. Consider your future income needs, gift and estate taxes, and the impact of your decisions on family members who may or may not be involved as the next generation of owners.

- Engage in a management buyout. If your family members aren’t able or willing to take the reins, a management buyout offers these key advantages: you save time and resources that would otherwise be spent finding an outside buyer, and the new owners have a shorter learning curve that positions them well to maintain the pace of business—providing for a smooth transition that ultimately funds your buyout.

- Set up an employee stock ownership plan (ESOP). These enable your employees to become owners through a qualified retirement plan and to purchase stock in your company. According to the National Center for Employee Ownership, about two-thirds of ESOPs are used to provide a market for the shares of a departing owner.

- Pursue an outside sale. If opportunity knocks on your door and the right buyer finds you, you may be able to sell your business at a premium. Whether you plan to sell your business in two or 20 years, you can increase your odds of getting a great price by understanding the current and future value of your business and the ideal entity structure, then taking the time and steps required to get your business into sale-ready condition.

Ownership Transition

If you intend to exit or transition the business to new ownership, consider your planning options well in advance—not only because planning can be financially rewarding but also because it can give you peace of mind.

- Integrate your business and personal strategies. A comprehensive plan will address business financial planning, personal financial planning, management succession, estate planning, and ownership transition together.

- Consult with your advisor on the sale of a subsidiary. If you’re considering the sale or transfer of a wholly owned subsidiary of your organization, determine with your advisor if the subsidiary has made any tax elections that would affect the taxability of the transfer. This is particularly important in situations involving a subsidiary that’s either a single-member LLC or an S corporation.

Contact Us

(800) 243-4936 | taxplanning@mossadams.com

Print the PDF

About Moss Adams

Nationwide, Moss Adams and its affiliates provide insight and expertise integral to your success.

Moss Adams LLP is a national leader in assurance, tax, consulting, risk management, transaction, and private client services.

Moss Adams Wealth Advisors LLC provides investment management, personal financial planning, and insurance strategies to help you build and preserve your wealth.

Tax planning offered by Moss Adams LLP. Investment advisory and personal financial planning services offered by Moss Adams Wealth Advisors LLC. Insurance management and consulting services offered by Moss Adams Securities & Insurance LLC.