Many US business owners, especially those that manufacture in the US and sell outside the US, don’t take advantage of the available US income tax export incentives. Given these tax breaks could result in a significant reduction in the federal income tax rate on exports, business owners would be well-served to evaluate the potential tax savings available to their businesses.

Any US business owner who exports may be able to utilize the interest-charge domestic international sales corporation (IC-DISC) or the foreign-derived intangible income (FDII) incentives.

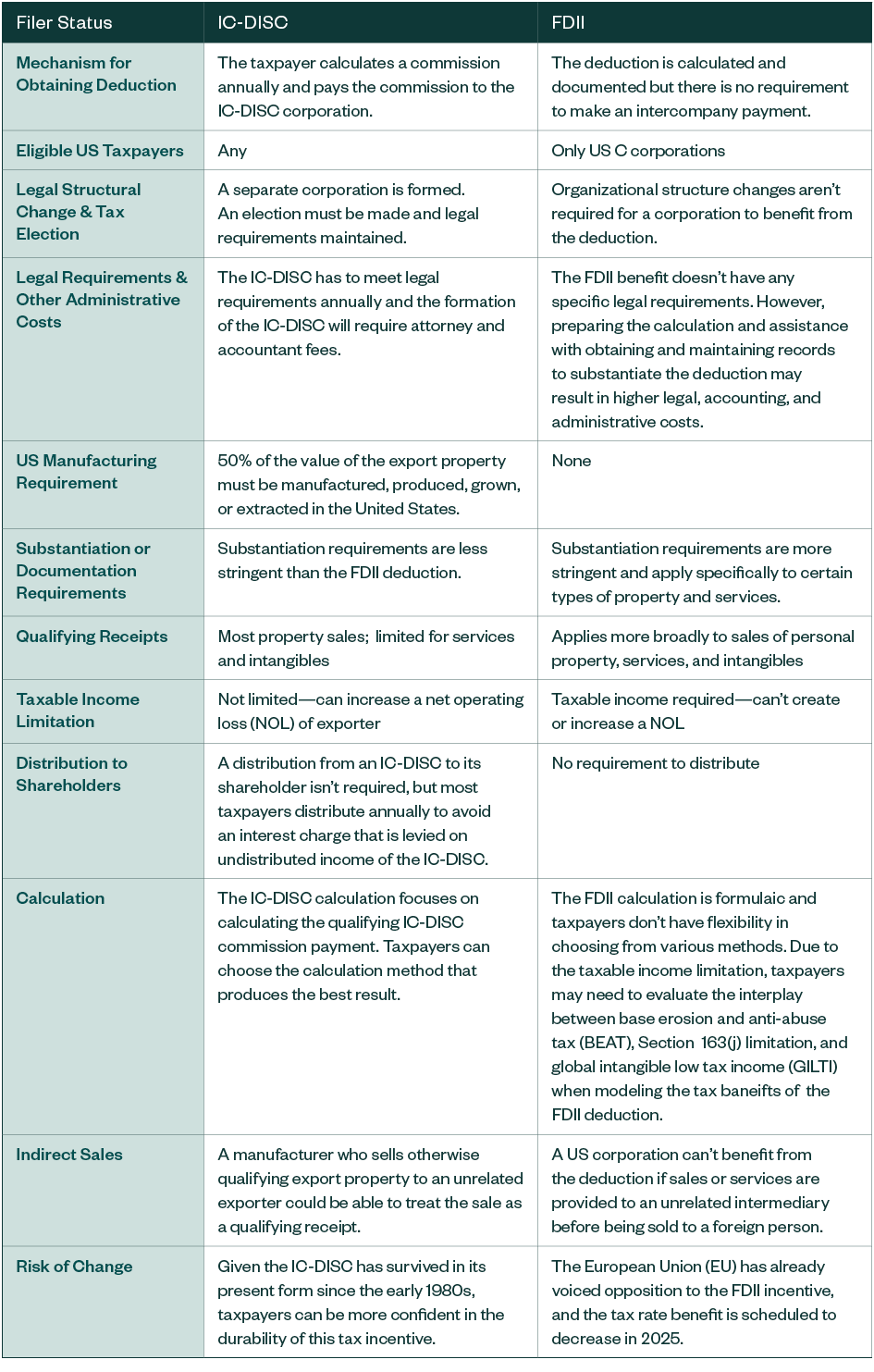

Below is a breakdown and comparison of each incentive including scenarios where both could be applicable in the same tax year.

How can a taxpayer use the IC-DISC incentive?

An IC-DISC is a US domestic corporation that meets certain requirements under US tax law and has made a valid IC-DISC election.

The IC-DISC incentive is available to almost any US taxpayer—individuals, C Corporations, S Corporations, partnerships, or LLCs—as long as they have qualifying exports.

A taxpayer who has established an IC-DISC annually identifies their qualifying exports and calculates a commission payment to the IC-DISC. Taxpayers have flexibility to choose the commission payment calculation method that provides the highest tax savings.

Taxpayers need to consider the following steps for the IC-DISC incentive:

- Determine if they have products that are qualifying exports—generally 50% or greater US manufactured or produced goods or services.

- Review historical financial information, and prepare an estimate of the tax benefit.

- Organize a US corporation that meets the formal legal requirements for an IC-DISC election.

- On an annual basis, calculate the qualifying commission payment to the IC-DISC.

When calculating the potential cash-savings, taxpayers should also consider the legal and maintenance costs of an IC-DISC.

How can a taxpayer use the FDII incentive?

Qualifying US corporations organized in the US can take advantage of the FDII deduction. The deduction is only available for tax years beginning after December 31, 2017.

To the extent a US corporation can substantiate its qualifying income—earned from the sale of property or services provided for foreign use or for royalties for intellectual property used outside the US —that income may benefit from a 37.5% deduction. The deduction is scheduled to decrease to 21.875% in 2025.

For more details, please see Final Regulations on FDII Deduction Provide Favorable Guidance.

How do the IC-DISC and FDII incentives compare to one another?

The chart below provides a side-by-side comparison of both incentives.

Can FDII and IC-DISC be used in the same tax year?

C corporations that have an IC-DISC, or may be interested in forming an IC-DISC, could also qualify for the FDII deduction. The Internal Revenue Code doesn’t prevent a C corporation that otherwise qualifies for both tax benefits from deducting both the IC-DISC commission and Section 250 deduction in the same tax year.

However, formulaically, the IC-DISC commission payment would reduce a C corporation’s foreign-derived deduction-eligible income when the benefit is being claimed on the same transaction.

We’re Here to Help

If you have any questions about how your company can benefit from export tax incentives, please contact your Moss Adams professional.

For more details, please see Turning Food, Beverage, and Agribusiness Exports into Tax Benefits: IC-DISCs and How to Increase Your Savings and Boost the Benefits of an IC-DISC with Accounts Receivable Factoring.