In late December 2020, the US Office of Management and Budget (OMB) released OMB Compliance Supplement addendum guidance for auditors that details the new audit requirements of the Single Audit Act for COVID-19-related programs, such as the Department of Treasury’s Coronavirus Relief Fund (CRF).

Gain insight into the following OMB addendum requirements below:

- Allowable costs and activities

- Subrecipient monitoring

- Schedule of Expenditures of Federal Awards (SEFA) reporting and disclosures

- Federal Funding Accountability and Transparency Act (FFATA) reporting

Allowable Costs and Activities

Auditors are required to follow the Treasury guidance and FAQs to evaluate if costs charged to the CRF program meet allowability requirements, which generally fall under the following three criteria:

- Necessary due to the public health emergency

- Not accounted for in a Tribe’s most recently approved budget as of March 27, 2020

- Incurred during the period of March 1, 2020, through December 31, 2021

The OMB clarified that an auditor may conclude a Tribe is compliant with a requirement based on the guidance that was in effect at the time of the activity or transaction. This is great news, given the frequency and amount of changes the Treasury made to its FAQs and guidelines over the course of the last year.

For example, some Tribes provided individual assistance to their citizens based on the Treasury’s guidance and FAQs as of April 22, 2020. The Treasury released new FAQs on June 24, 2020, which specified the requirement of performing an assessment of individual need before providing assistance. Auditors may take into account the timing of when a Tribe decided to pay citizens when determining the Tribe’s compliance with Treasury guidance.

Certain Costs and Activities

Below are a few items of significance regarding allowable costs and activities.

Hazard Pay

The Treasury indicates that a Tribe can charge hazard pay to CRF only if both of the following apply:

- An employee is performing hazardous duty or work involving physical hardship

- The hazardous duty or physical hardship work is related to COVID-19

Typically, employees who aren’t working on COVID-19-related matters and aren’t required to interact with the general public won’t qualify for hazard pay—even if they’re considered essential workers and had to go into the office during the pandemic.

Equipment, Vehicles, and Real Property

If a Tribe purchased equipment, vehicles, or real property with funding from the CRF program, OMB emphasized there must be documentation showing it was more cost effective to purchase the asset versus leasing or improving an existing property.

Construction

Although the Consolidated Appropriations Act, 2021 extended the use of CRF funds to December 31, 2021, Treasury guidance requires any construction projects paid from the fund be necessary due to COVID-19 and in response to the current pandemic.

We don’t know when the World Health Organization will no longer consider COVID-19 a pandemic, which means each Tribe should determine a reasonable timeframe for completing construction projects during 2021. This will allow them to be placed in service during the current COVID-19 pandemic.

Subrecipient Monitoring

Difference Between Beneficiaries and Subrecipients

If a Tribe provided CRF money to another Tribal entity and is unsure whether the entity qualifies as a subrecipient or beneficiary, refer to the letter the Treasury provided to Tribes and posted on NAFOA’s web site. When determining whether an entity is a beneficiary or subrecipient, consider focusing on the substance and nature of the transaction to make your determination.

Beneficiary

If a Tribe provided CRF money to a Tribal entity—such as an enterprise, component unit, or not-for-profit organization—as a direct assistance payment rather than to operate a program on behalf of the Tribe, that entity could be considered a beneficiary.

Treasury states that subrecipients don’t include individuals and organizations—such as businesses, not-for-profits, or educational institutions—that are beneficiaries of an assistance program established using payments from CRF.

For example, if a Tribe provided CRF assistance to its casino to cover operational costs when the casino was closed due to the pandemic, the casino would likely be considered a beneficiary. Treasury states that a beneficiary isn’t subject to the Single Audit Act.

Subrecipient

If a Tribe provided CRF money to a Tribal entity to operate a program on behalf of the Tribe, that entity would be considered a subrecipient.

For example, if a Tribe provided CRF assistance to its legally separate housing authority to operate a new COVID-19 emergency rental-assistance program on behalf of the Tribe, the housing authority would be considered a subrecipient. If a subrecipient spends over $750,000 of federal funds, it would be subject to the Single Audit Act.

What Happens if a Tribe Has Subrecipients

If a Tribe has subrecipients, the auditor will most likely test the Tribe’s compliance with subrecipient monitoring. In accordance with Uniform Guidance, the Tribe should take the following steps for subrecipient monitoring:

- Provide the federal award information to the subrecipient, including all applicable award requirements.

- Evaluate the subrecipient’s risk of noncompliance with federal requirements based on the subrecipient’s prior experience with similar subawards, results of previous audits, changes in personnel or systems, and the extent and results of any federal awarding agency monitoring.

- Perform monitoring activities over the subrecipient’s compliance with its federal program requirements, including reviewing financial and programmatic reports, following up on actions taken to resolve deficiencies, and issuing management decisions for any audit findings related to the federal award.

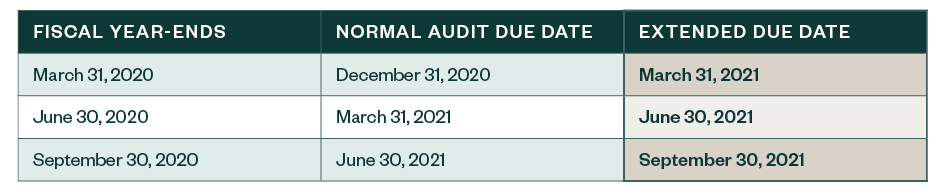

Extension of Audit Deadlines

In late December 2020, the OMB addendum provided an automatic three-month audit submission extension for Single Audits of 2020 year-ends through September 30, 2020, year-ends, for all entities that received COVID-19 funding.

If a Tribal entity used the extension, it should document the reason for the delayed audit submission.

Current Deadline Extensions for Common Fiscal Year-Ends Granted in the Addendum

On March 19, 2021, OMB released a memo to federal agencies that allows a cognizant or oversight agency—which is the Department of the Interior for Tribes—to provide entities that have fiscal year-ends through June 30, 2021, and who haven’t yet filed their audit reports, a six-month extension beyond their normal due date. For this extension to apply, an entity doesn’t need to have received COVID-19 funding.

SEFA Reporting and Disclosures

In addition to the SEFA changes reported in our November 2020 TFQ, there are two more SEFA changes to be aware of as a result of the information included in this addendum.

Provider Relief Funds

If a Tribe, Tribal hospital, or Tribal health facility has a fiscal year-end before December 30, 2020, and received Provider Relief Funds (PRF) from the Department of Health and Human Services (HHS), it wouldn’t report PRF expenditures or lost revenue on the 2020 fiscal year SEFA. Those expenditures would instead be reported in the 2021 fiscal year SEFA.

Tribal entities with fiscal years ending on or after December 31, 2020, would report allowable expenditures and lost revenue on the SEFA, which generally should tie to amounts reported to HHS on the use of PRF funds. Those reporting requirements haven’t yet been finalized, however, so stay tuned for any changes.

Donated Personal Protective Equipment

If a Tribe received donated personal protective equipment (PPE) that was originally purchased with federal assistance funds, there should be a separate footnote to the SEFA indicating the fair market value of the PPE at the time of receipt.

Donated PPE has no bearing on the Single Audit and can be marked as unaudited, in which case auditors shouldn’t require justification for how the fair market value was determined.

FFATA Reporting

OMB has added a FFATA reporting requirement in the OMB addendum. It requires Tribes and Tribal federal contractors that provide $25,000 or more in first-tier subawards or subcontracts to perform monthly reporting through the FFATA Subaward Reporting System.

While FFATA reporting doesn’t apply to the CRF program, auditors will need to test any other COVID-19 programs where FFATA reporting does apply.

Additionally, for Single Audits of fiscal year-ends after September 30, 2020, auditors are required to test FFATA reporting for all major federal programs for which this reporting is applicable.

We’re Here to Help

For help navigating the new requirements or the related deadline extensions, contact your Moss Adams professional.