The new lease accounting guidance impacts the construction industry in potentially unexpected ways.

Although the general provisions of the guidance and its application in many instances are straightforward, there are certain construction-specifics scenarios to consider, such as whether or not there are embedded leases within subcontractor or other arrangements and whether the amortization of leased assets used on a construction site should be included in project costs.

But first, let’s cover some basics.

Updates to Lessee Accounting for Leases

The new lease accounting standard intends to provide users of financial statements with greater visibility and transparency into the financial impacts of a lessee’s lease obligations and leased assets.

Lessees are required to recognize all leases of property or equipment on their balance sheet. However, many will likely adopt an optional practical expedient whereby leases with terms of 12 months or less aren’t recognized as assets and liabilities on the lessee’s balance sheet but rather accounted for as executory contracts—similar to how operating leases were accounted for prior to the Financial Accounting Standards Board’s (FASB) new lease accounting guidance.

This may affect how an entity is evaluated by the users of its US generally accepted accounting principles (GAAP) financial statements such as banks, investors, board members, and other stakeholders across a myriad of industries, including construction.

Effective Dates

The FASB published accounting standards updated (ASU) 2016-02, Leases (Topic 842) in February 2016, which created accounting standards codification (ASC) Topic 842, Leases. Since issuing ASU 2016-02, the FASB deferred the effective dates of ASC Topic 842 for certain entities.

In June 2020, the FASB acknowledged that entities could face limited resources due to the COVID-19 pandemic and provided an additional one-year deferral of the effective date for certain entities. However, more recently the FASB made it clear that no further deferrals should be expected.

ASC 842 is effective for private companies for fiscal years beginning after December 15, 2021 and interim periods within fiscal years beginning after December 15, 2022. Although the reporting date for reflecting the adoption fast approaches, many construction companies have yet to start preparing to adopt this new accounting standard.

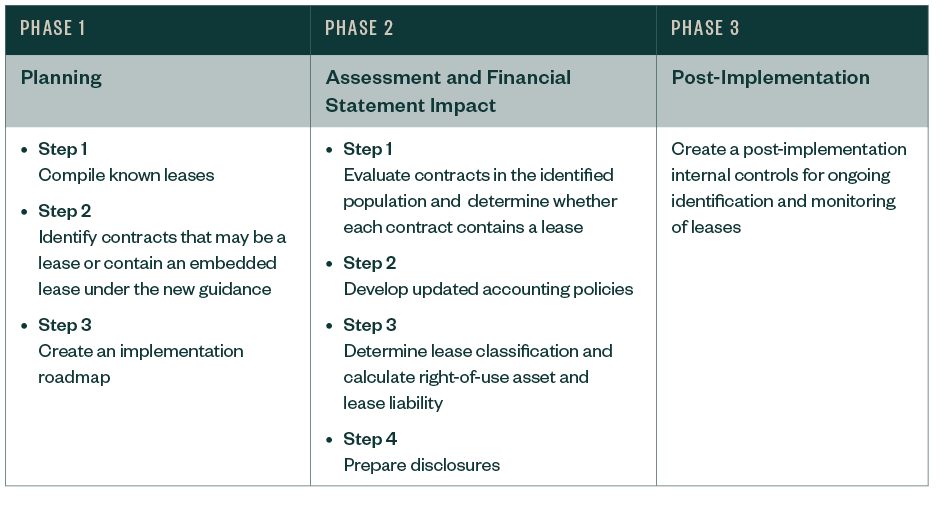

Three-Phased Approach to Implementation

As your business organizes its adoption approach, explore a step-by-step process broken into three phases.

Key Considerations for Construction Companies to Adopt the Leasing Standard

There are many conditions to consider for construction companies.

1. Are Your Leased Assets in Scope of the Standard?

The first step to adopting the lease standard is to determine all arrangements that are within scope of ASC 842.

There are two criteria for an arrangement to be or contain a lease:

- Implicitly or explicitly identifies specific property, plant or equipment (identified asset)

- Conveys the right to control the identified asset for a period in exchange for consideration

2. Does Your Company Have Any Embedded Leases?

For many leases, that first step is straightforward. However, the possibility of embedded leases must also be considered.

For example, oftentimes contractors have service contracts that include the use of specific equipment, for example cranes and job site offices.

Even if the given contract never mentions the word “lease,” and it appears to be a supply arrangement or a service contract, if the arrangement conveys control of the specific asset which is physically distinct, and the provider cannot easily substitute a different asset in its place, then it may be an embedded lease that must be accounted for in accordance with ASC 842.

Identification of embedded leases have been widely noted as one of the most time-consuming aspects of implementing the new lease accounting standard by public companies and others who have already adopted the new standard.

3. How Does the Lease Accounting Standard Impact Your Balance Sheet?

The biggest change from legacy GAAP for construction, like other industries, is the impact to the balance sheet.

Specifically, operating leases that were historically omitted from the balance sheet, will now be recognized through a right-of-use asset, along with the recording of an associated lease liability.

However, construction companies will also want to consider if it’s appropriate for the amortization and interest expense incurred on the lease liabilities to be included within job costs for purposes of recognizing revenue over time for those performance obligations for which progress towards satisfaction is measured using an input method of costs incurred to date compared to total estimated costs (commonly referred to as “percentage-of-completion”).

4. Does the Lease Accounting Standard Impact Key Financial Decisions?

Yes, key financial decisions will also be impacted as a result of adopting ASC Topic 842.

For example, construction companies may want to consider:

- The duration of new lease obligations

- Whether to purchase outright certain assets that were historically leased under operating leases

- Whether bank covenants—certain ratios, for example—are impacted by the recognition of the right-of-use assets and lease liabilities for previously unrecognized operating leases

- If inclusion of an operating lease’s lease expense and a finance lease’s amortization and interest expense in job costs is appropriate, how will it impact the overall profitability of projects

We’re Here to Help

For more information about the new lease standard, refer to our guide: ASC Topic 842, Leases: The FASB’s New Guidance and Their Effect on Leasing Arrangements.

For additional questions or help understanding how the new standard may affect your business, contact your Moss Adams professional.

You can also learn more about our Construction Practice and additional topics affecting the industry.