How Wineries, Breweries, and Distilleries Can Claim the R&D Tax Credit

A version of this article previously appeared in the September–October 2017 issue of Spirited magazine.

Wineries, breweries, and distilleries continuously develop new or improved products and processes—from new product formulations and equipment design to new fermentation techniques and packaging processes. These activities can qualify for the R&D tax credit, saving them up to 10% of annual R&D costs for federal purposes and much more when state credits are factored in. However, many producers of alcoholic beverages aren’t claiming the credit because of misconceptions about who can claim it and for what kind of work.

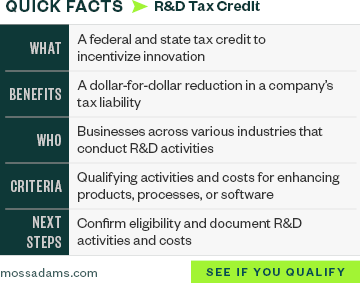

What’s the R&D Tax Credit?

The federal R&D tax credit is a dollar-for-dollar tax savings that directly reduces a company’s regular tax liability. There’s no limitation on the amount of expenses and credit that can be claimed each year. If the R&D credit can’t be used immediately or completely, any unused credit can be carried back one year or carried forward for up to 20 years. Additionally, over 30 states offer R&D tax credit incentives to further increase a company’s savings.

In general, the R&D credit claim is approximately 6%–10% of a company’s qualified expenses, depending on several factors. Generally, the more a company spends on qualified R&D, the higher the credit it’ll receive, with taxpayers receiving a larger credit if they increase R&D spending year-over-year. The savings could be even greater if that company is also performing R&D in a state that offers an R&D credit.

What Types of Activities Qualify for the R&D Tax Credit?

The R&D tax credit isn’t limited to the work of scientists or dedicated R&D laboratories. Most producers of alcoholic beverages perform qualifying R&D activities as part of their normal operations.

Some examples of activities that may be eligible for the R&D tax credit include developing, designing, or testing new or improved:

- Product recipes for flavor, texture, and aroma profiles

- Product formulations, such as ready-to-drink or low alcohol by volume (ABV)

- Heating techniques and enzymes for mash

- Fermentation techniques and yeast strains

- Equipment design such as stills, tanks, crushing, sorting, and bottling

- Automated processes

- Filtration or straining methodologies

- Bottling and packaging processes

- Methods for consistency, stability, and shelf life

- Methods for sustainability

- Software applications

What Types of Expenses Qualify for the R&D Tax Credit for Wineries, Breweries, and Distilleries?

Most qualifying expenses fall into three categories:

- Wages

- Supplies

- Contractor expenses

Wages

Qualifying employee wages can include Form W-2, Box 1, or pass-through income subject to self-employment tax. This would include individuals performing qualified research as well as those that directly support or supervise the research. The rules specify if an employee is 80% qualified, 100% of their wages can be included to calculate the credit.

Some examples of eligible staff include the following.

- A winemaker, brewer, or distiller who’s driving new product or process development

- Engineers, technicians, or fabricators developing new equipment

- Production or cellar staff crafting test batches and prototypes

- Lab or quality assurance personnel testing new products

Supplies

Qualified supplies include tangible property used in the qualified research, such as:

- Ingredients

- Enzymes

- Yeast

- Lab equipment and supplies

Qualified supplies may also include:

- Small- or large-scale test batches

- Prototypes

- Pilot models

Contractor Expenses

Payments to contractors may also be eligible, but they’re subject to some restrictions.

Qualified contractor expenses typically include the following.

- Consultants

- Temporary labor

- Outside testing

- Other third-party services

What Documentation Is Necessary for the R&D Tax Credit?

With recent increases in IRS scrutiny around R&D credits, it’s crucial to understand what’s necessary to substantiate a credit claim. Like many other aspects of tax compliance, documentation is important for both the quantitative and qualitative aspects of the R&D tax credit.

From a quantitative perspective, taxpayers should maintain documentation for employee wages, specifically Form W-2 data, as well as general ledger detail for any supplies or contract research related to R&D. Ideally, these amounts should be tracked by project, account, and vendor and be easily identifiable within the general ledger.

From a qualitative perspective, taxpayers should retain all formal and informal documentation created during the R&D, such as:

- Project descriptions or plans

- Trial designs

- Test logs and reports

- Sensory and organoleptic evaluations

- Chemical analysis

- Notes, presentations, and emails

We’re Here to Help

Each company’s goals and resources are unique, which makes it important to develop a customized project plan to identify, calculate, and support your company’s R&D tax credits. To learn more about R&D tax credits, request a complimentary credit benefit estimate to see how much your company could save.